Introduction

The purpose of this article is to present the key changes introduced by the instant payment Regulation.

Of course, this regulation does not exist in a vacuum. Because of that, I think it may be valuable, to begin with a few words about SEPA payments in general (without going into much detail) so that we get a bit of the context in which this regulation appeared.

So, what is SEPA?

The Single Euro Payments Area (SEPA) is a European Union (EU) initiative to harmonise euro payments. SEPA covers only transactions denominated in euro.

Thanks to this project, citizens experience the same ease and convenience when making cross-border euro transactions as they do when paying within their home country.

The main idea of SEPA is that payments within and across national boundaries are processed under the same basic conditions and following the same rights and obligations.

In other words, the same rules and reachability apply to national and cross-border credit transfer transactions.

It is also true in the context of pricing policy.

Charges levied by a Payment Service Provider (PSP) on a Payment Service User (PSU) in respect of cross-border payments shall be the same as charges levied by that PSP for corresponding national payments of the same value. In other words, the pricing of euro cross-border payments is aligned with those of local transactions.

When it comes to charges, it is also important to note that they are based on the shared principle such that the Originator and Beneficiary are charged separately and individually by the Originator PSP and Beneficiary PSP respectively. Additionally, charges are not deducted from the amount transferred (except for explicit agreement between the Beneficiary and Beneficiary PSP in this respect).

In the SEPA context, where the payer’s PSP and the payee’s PSP are located in different countries we are talking about ‘cross-border payment transaction’. If they are located in the same country, we are talking about ‘national payment transaction’.

But, what are the countries eligible for SEPA payments (SEPA countries)?

Although SEPA is a European Union (EU) initiative, the geographical scope of the SEPA schemes is broader than the European Union and currently covers 36 countries and territories: the 27 EU Member States plus United Kingdom, Iceland, Norway, Liechtenstein, Switzerland, Monaco, San Marino, Andorra and Vatican City State/Holy See (see the related document the interactive map).

To make SEPA payment both the payer’s PSP and the payee’s PSP must be located in SEPA countries. To cover payments with a larger scope, the One-Leg Out Instant Credit Transfer scheme was introduced (learn more). This is not, however, a SEPA scheme.

As SEPA payments have been with us for a while, lots of information about SEPA is available online.

Official information, however, we can find on the EPC website: https://www.europeanpaymentscouncil.eu/

What is ECP?

The European Payments Council is an international not-for-profit association of Payment Service Providers (PSPs). The primary task of the EPC is to manage five payment schemes.

Four of these are SEPA schemes:

- The SEPA Credit Transfer scheme.

- The SEPA Instant Credit Transfer scheme.

- The SEPA Direct Debit Core scheme.

- The SEPA Direct Debit Business-to-Business scheme.

The fifth is The One-Leg Out Instant Credit Transfer scheme I mentioned above.

Last but not least, other important aspects of SEPA payments I would like to mention are:

- The payment account identifier must be in the format of IBAN.

- In addition to payee’s IBAN, the payer is not required to provide PSP BIC ( ‘IBAN only’ rule).

- Payment messages are in ISO 20022 XML format.

Instant payment regulation

As we have seen, one of the already existing SEPA schemes refers to instant payments (The SEPA Instant Credit Transfer scheme). It means that instant payments in euro are not new in the EU.

Nevertheless, the new Regulation will significantly change instant payments landscape, by making them fully available.

In short, the instant payments Regulation will allow people to transfer money within ten seconds at any time of the day, including outside business hours, not only within the same country but also to another SEPA country.

The new rules will come into force after a transition period that will be faster in the euro area and longer in the non-euro area.

The timelines are ambitious. They are presented in the two diagrams at the end of this article.

The new Regulation was published in the EU’s Official Journal on 19.03.2024 (Regulation (EU) 2024/886) and comes into force 20 days after (on 08.04.2024).

The Regulation is directly applicable in all Member States, without needing to be transposed into national law.

What is the relation between instant payment Regulation and other payments-related legal acts?

As the SEPA payments are not new, the instant payment Regulation amends already existing, following documents:

- SEPA regulation (Regulations (EU) No 260/2012)

- Regulation on cross-border payments in the Union (Regulation (EU) 2021/1230)

- PSD2 (Directive (EU) 2015/2366)

- Directive on settlement finality in payment and securities settlement systems Directive (Directive 98/26/EC)

Motivation

As instant payments in euro exist today why are any changes necessary?

The rationale behind the instant payment Regulation is that the efforts of the European payments industry have not proven sufficient to ensure a high uptake of instant payments at the EU level.

It is believed, that only a widespread and rapid increase in such uptake could unlock the full-scale network effects of instant credit transfers in euro.

Additionally, instant credit transfers in euro emerged on the market only after the adoption of the SEPA Regulation. It is therefore necessary to establish specific requirements applicable to instant payments, in addition to the general requirements applicable to all credit transfers.

Moreover, it is believed that the new rules will improve the strategic autonomy of the European economic and financial sector as they will help reduce any excessive reliance on third-country financial institutions and infrastructures.

So, what are the main provisions of the instant payment Regulation?

Here they are…

What is a retail payment system?

First of all, the new Regulation changed to the definition of the retail payment system.

According to this new definition “retail payment system” means a payment system the main purpose of which is to process, clear or settle credit transfers or direct debits which are primarily of small amount, and that is not a large-value payment system.

In the previous definition of “retail payment system” there was a reference to the fact that payments are bundled together for transmission. This is no longer the case.

The definition was amended to reflect the character of instant payments which are processed individually, on a one-by-one basis.

Access to Payment systems

What is also new, is the fact, that the instant payment Regulation grants access to payment systems for payment and e-money institutions, by changing the settlement finality Directive in this respect. Directive 98/26/EC is amended in order to include payment institutions and electronic money institutions in the list of entities which fall under the definition of the term ‘institution’ in that Directive, but only for the purpose of defining participants of a payment system.

It is believed, that payment institutions and electronic money institutions will contribute to facilitating the uptake of instant credit transfers in euro and should therefore be subject to the requirements of this amending Regulation.

As a result, these entities will also be covered by the obligation to offer the service of sending and receiving instant credit transfers, after a transitional period (see next point of the article).

The Regulation includes appropriate safeguards to ensure that the access of those entities to payment systems doesn’t carry additional risk to the system.

Mandatory scheme

Before instant payment Regulation SCT Inst scheme was optional.

This is going to change.

According to the new rules PSPs such as banks, which provide standard credit transfers in euro, will be required to offer to all of their PSUs also the service of sending and receiving instant payments in euro.

This requirement should apply with respect to all payment accounts that PSPs maintain for their PSUs. In other words, PSPs shall ensure that all payment accounts that are reachable for regular credit transfers are also reachable for instant credit transfers 24 hours a day and on any calendar day.

It is believed, that ensuring that all PSUs are able to initiate and receive instant credit transfers in euro is a precondition for an increased uptake of such transactions.

What are the deadlines for this requirement?

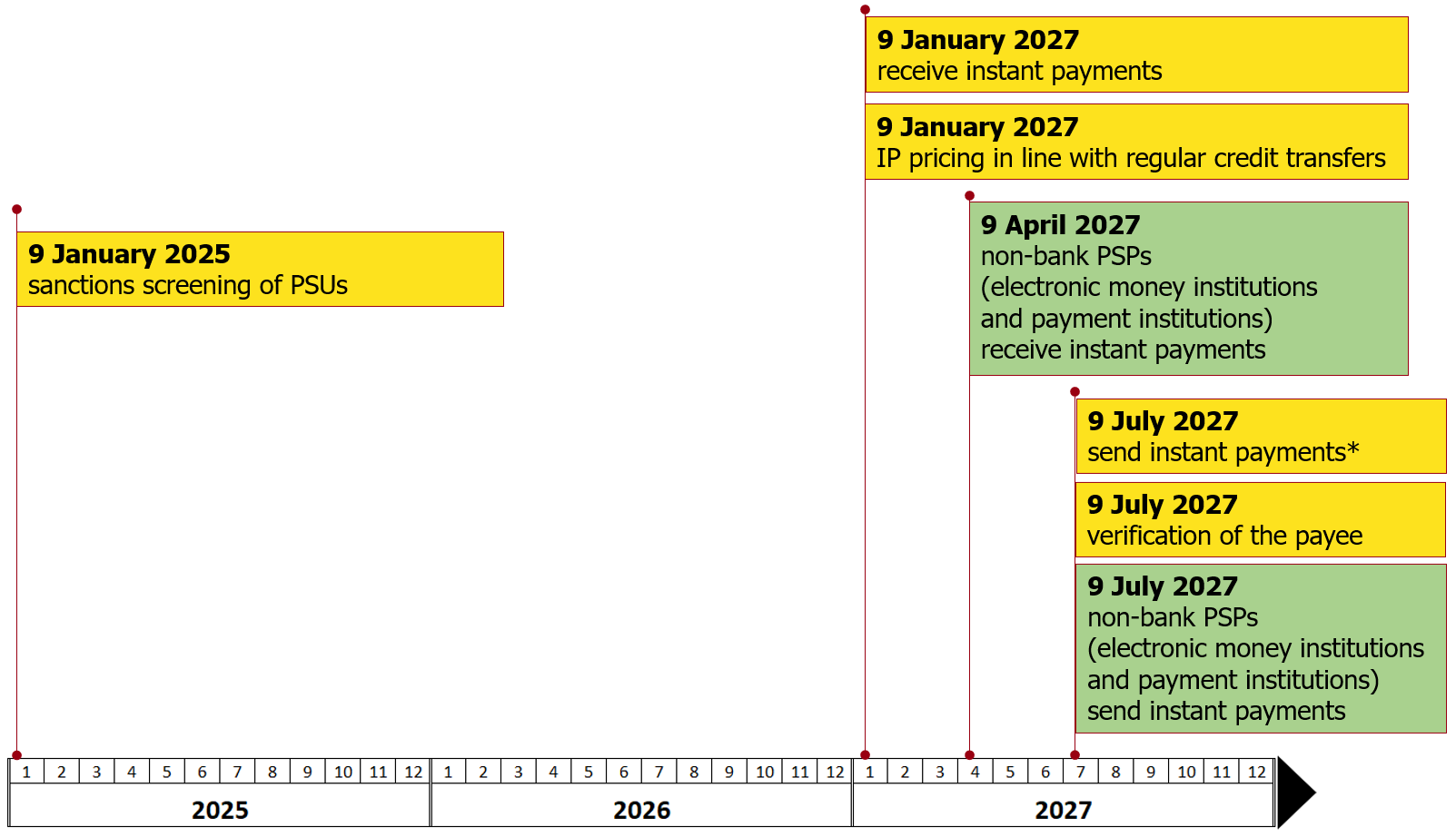

PSPs that are located in a Member State whose currency is the euro shall offer PSUs the payment service of receiving instant credit transfers in euro by 9 January 2025, and the payment service of sending instant credit transfers in euro by 9 October 2025.

PSPs that are located in a Member State whose currency is not the euro shall offer PSUs the payment service of receiving instant credit transfers in euro by 9 January 2027, and the payment service of sending instant credit transfers in euro by 9 July 2027. By way of derogation until 9 June 2028 PSPs that are located in a Member State whose currency is not the euro shall not be obliged to offer PSUs the payment service of sending instant credit transfers in euro from payment accounts denominated in the national currency of that Member State, during the time when those PSPs neither send nor receive non-instant credit transfer transactions in euro with respect to such accounts.

PSPs that are electronic money institutions or payment institutions and that are located in a Member State whose currency is the euro shall offer PSUs the payment service of sending and receiving instant credit transfers in euro by 9 April 2027.

PSPs that are electronic money institutions or payment institutions and that are located in a Member State whose currency is not the euro shall offer PSUs the payment service of receiving instant credit transfers in euro by 9 April 2027 and the payment service of sending instant credit transfers in euro by 9 July 2027.

Pricing policy

Until now, the approach to instant payment pricing policy was not uniform. Some markets placed instant payments as a premium service.

With the new Regulation, the charges that apply for instant credit transfers (if any) must not be higher than the charges that apply for credit transfers of corresponding type.

It means that all types of charges applied to payers and payees for the execution of instant credit transfers in euro should not exceed such charges applied to the same PSU for corresponding types of other credit transfers in euro.

This provision aims to ensure that, from the PSU’s perspective, it is not more expensive to send or receive an instant credit transfer in euro than it is to send or receive a non-instant credit transfer in euro provided with the same additional features or services. In particular, PSPs offering different variants of a payment solution where the only distinguishing characteristic between them would be the use of instant credit transfers in one and non-instant in the other, should ensure that the total charge for the instant credit transfer is not higher than the charge for the non-instant credit transfer.

What are the deadlines for this requirement?

PSPs located in a Member State whose currency is the euro shall comply by 9 January 2025.

PSPs located in a Member State whose currency is not the euro shall comply by 9 January 2027.

Charges for additional services

However, regardless of the previous point, PSPs should be able to decide on the charges for additional features or services on top of the underlying instant credit transfer.

An instant-credit-transfer-based payment solution encompassing additional features or services should not be considered to be of a corresponding nature to a non-instant credit transfer offered without the same additional features or services.

On the other hand, where a PSU can submit payment orders for non-instant credit transfers without any additional features or services, the same possibility should also be available for instant credit transfers.

The round-the-clock availability

The round-the-clock availability every day of the year is an intrinsic feature of instant credit transfers.

According to the definition, “instant credit transfer” means a credit transfer that is executed immediately, 24 hours a day and on any calendar day.

Currency of the transfer

As the name of the Regulation states, it refers to instant credit transfers in euro.

Currency of the accounts

The currency of the accounts involved in the transaction does not have to be denominated in euro. This does not change in comparison to the current rules of SCT Inst scheme.

Verification of the payee

This requirement will strengthen the protection of PSUs from sending funds to an unintended payee.

Under the new rules, instant payment providers will need to verify that the beneficiary’s IBAN and name match in order to alert the payer to possible mistakes or fraud before a transaction is made. What is important is that this requirement will apply to regular transfers too (not only to instant payments).

Under the new rules, PSPs should provide a service ensuring verification of the payee to whom the payer intends to send a credit transfer. The PSP should indicate to the payer the name of the payee associated with the payment account identifier provided by the payer in a manner that ensures compliance with GDPR.

To avoid undue friction or delays in the processing of the transaction, the payer’s PSP should perform such service immediately after the payer provides the relevant information about the payee and before the payer is offered the possibility of authorizing the credit transfer.

Additionally, the payer’s PSP shall offer this service regardless of the payment initiation channel used by the payer.

PSPs shall provide PSUs that are not consumers with the means to opt out from receiving the service ensuring verification when submitting multiple payment orders as a package. However, PSPs shall ensure that PSUs that opted out from receiving the service ensuring verification have the right to opt in at any time to receive that service.

Moreover, this should not result in PSUs incurring any additional charges or fees. In other words, the service related to this requirement shall be provided to all PSUs free of charge.

The service ensuring verification should as far as possible be carried out in accordance with an EU-wide set of rules and standards in order to encourage a smooth and interoperable implementation.

What are the deadlines for this requirement?

PSPs located in a Member State whose currency is the euro shall comply by 9 October 2025.

PSPs located in a Member State whose currency is not the euro shall comply by 9 July 2027.

Initiation channels

There exist a variety of payment initiation channels through which PSUs can place a payment order for a credit transfer in euro, for example, via online banking, a mobile application, an automated teller machine, a self-service terminal, in a branch or by phone. To ensure that all PSUs have access to instant credit transfers in euro, there should be no difference in terms of the payment initiation channels through which PSUs can place payment orders for instant credit transfers and other credit transfers.

As a consequence, according to the Regulation PSPs shall ensure that payers are able to place a payment order for an instant credit transfer through all of the same payment initiation channels as the ones through which those payers are able to place a payment order for other credit transfers.

Initiate as a package

In addition to the above requirement, where a PSU can submit multiple payment orders for credit transfers as a package, it should also be possible to submit multiple payment orders for instant credit transfers as a package.

In other words, when offering the payment service of sending and receiving instant credit transfers, PSPs shall offer their PSUs the possibility of submitting multiple payment orders as a package, if PSPs offer such possibility to their PSUs for other credit transfers.

Moreover, PSPs shall not impose limits on the number of payment orders that can be submitted in a package of instant credit transfers which are lower than the limits they impose in respect of packages of other credit transfers.

Where a PSU submits multiple payment orders for instant credit transfers as a package to its PSP, that PSP should immediately start to unpack that package to turn it into individual instant credit transfer transactions.

Immediately upon unpacking, the payer’s PSP should transmit that individual instant credit transfer transaction to the payee’s PSP.

Default route for payments?

The last two above points underline the possibility for PSPs to offer all credit transfers initiated by their PSUs as instant credit transfers by default.

Time of the receipt

Generally, the time of receipt of a payment order for an instant credit transfer shall be the moment it has been received by the payer’s PSP, regardless of the hour or calendar day.

When an instant credit transfer is submitted in a package of multiple payment orders, the time of receipt should be the moment when the individual instant credit transfer transaction has been unpacked. In such scenario, the payer’s PSP shall start the conversion of the package immediately after it has been placed by the payer and complete that conversion as soon as possible.

Since some payment initiation channels, such as bank retail locations, are not available round the clock, the time of receipt of a paper-based payment order (non-electronic payment order) for an instant credit transfer should be the moment when the paper-based payment order is introduced into the internal system of the payer’s PSP, which should occur as soon as such payment initiation channels are available.

Additionally, where a payment order for an instant credit transfer in euro is submitted from a payment account that is not denominated in euro, the time of receipt of that payment order should be the moment when the amount of the payment transaction has been converted into euro. Such currency conversion shall take place immediately after the payment order has been placed by the payer.

Execution Time

The instant payments Regulation allows people to transfer money within ten seconds at any time of the day, including outside business hours.

The process should be as follows:

- Immediately after the time of receipt of a payment order for an instant credit transfer, the payer’s PSP shall verify whether all of the necessary conditions for processing the payment transaction are met and whether the necessary funds are available,

- If verification is positive, PSP shall reserve or debit the amount of the payment transaction from the account of the payer, and immediately send the payment transaction to the payee’s PSP.

- The payee’s PSP shall, within 10 seconds of the time of receipt of the payment order for an instant credit transfer by the payer’s PSP, make the amount of the payment transaction available on the payee’s payment account in the currency in which the payee’s account is denominated and confirm the completion of the payment transaction to the payer’s PSP.

- Where the payer’s PSP has not received a message from the payee’s PSP confirming that the funds were made available on the payee’s payment account within 10 seconds of the time of receipt, the payer’s PSP shall immediately restore the payment account of the payer to the state in which it would have been had the transaction not taken place.

Confirmation for the payer

Immediately upon receiving the confirmation of completion, or where no such confirmation of completion is received by the payer’s PSP within 10 seconds of the time of receipt of the payment order for an instant credit transfer, the payer’s PSP shall, free of charge, inform the payer, as well as, where applicable, the payment initiation service provider, whether the amount of the payment transaction has been made available on the payee’s payment account.

Credit value date

The payee’s PSP shall ensure that the credit value date for the payee’s payment account is the same date as the date on which the payee’s payment account is credited by the payee’s PSP.

Limit for instant payments

According to the rules set by the Regulation, in order to allow PSUs greater discretion when making use of instant credit transfers, a PSU should be able to set an individual limit fixing a maximum amount, either on a daily or per transaction basis, that it can send by means of instant credit transfer. PSUs should be able to modify or lift those individual limits at any time, without difficulty, and with immediate effect.

Where a PSU’s payment order for an instant credit transfer exceeds the maximum amount, the payer’s PSP shall not execute the payment order for the instant credit transfer, shall notify the PSU thereof, and shall inform the PSU how to modify the maximum amount.

Screening of PSUs against EU sanctions lists

With the instant payment Regulation, there is a change in the way sanction screening is applied.

PSPs should no longer apply transaction-based screening. In other words, during the execution of an instant credit transfer, the PSPs shall not verify whether the payer or the payee are persons or entities subject to targeted financial restrictive measures.

This will remove frictions from instant payment settlement.

On the other hand, the screening should be applied to PSUs. As the Regulation states, PSPs should periodically, and at least daily, verify whether their PSUs are persons or entities subject to targeted financial restrictive measures.

Timelines

The new rules will come into force after a transition period that will be faster in the euro area and longer in the non-euro area.

Below are the deadlines applicable to both groups.

PSPs located in a Member State whose currency is the euro

The green color highlights the deadlines for PSPs being electronic money institutions or payment institutions.

PSPs located in a Member State whose currency is not the euro

The green color highlights the deadlines for PSPs being electronic money institutions or payment institutions.

*By way of derogation, until 9 June 2028 PSPs located in a Member State whose currency is not the euro shall not be obliged to offer PSUs the payment service of sending instant credit transfers in euro from payment accounts denominated in the national currency of that Member State, during the time when those PSPs neither send nor receive non-instant credit transfer transactions in euro with respect to such accounts.